Macroeconomics

April 2023

As the world emerges from the Covid-19 pandemic, rising prices that resulted from a period of expansionary monetary policy and other economic forces have resurfaced an age-old macroeconomics question: Is inflation progressive or regressive, and who does it hurt the most?

In new work that uses a wealth of data to model how inflation affects households of different ages and with different levels of education (PDF), researchers from Princeton and Columbia Business School argue that inflation is neither universally regressive or progressive, and the specific circumstances of the shock matter.

In an important methodological contribution, they demonstrate that two factors play a critical role in determining who wins and loses when prices go up. First, the source of inflation matters. Second, they show that the effect of inflation on changes in household income relative to change in prices, rather than on prices alone, must be considered. The authors’ new method can identify households whose incomes rise along with prices, thereby muting the effects of inflation on those households, as well those whose incomes remain stagnant or decline.

Applying their new methodology to the study of two different inflationary shocks, they show that the effect of a shock on asset prices is the most significant determinant of whether an inflationary shock is regressive or progressive.

The authors study two major drivers of inflation. The first is an oil shock, where prices increase because of a decrease in the supply of oil. The second is an expansionary monetary policy shock, where prices increase as a result of interest rate cuts or other aspects of monetary policy.

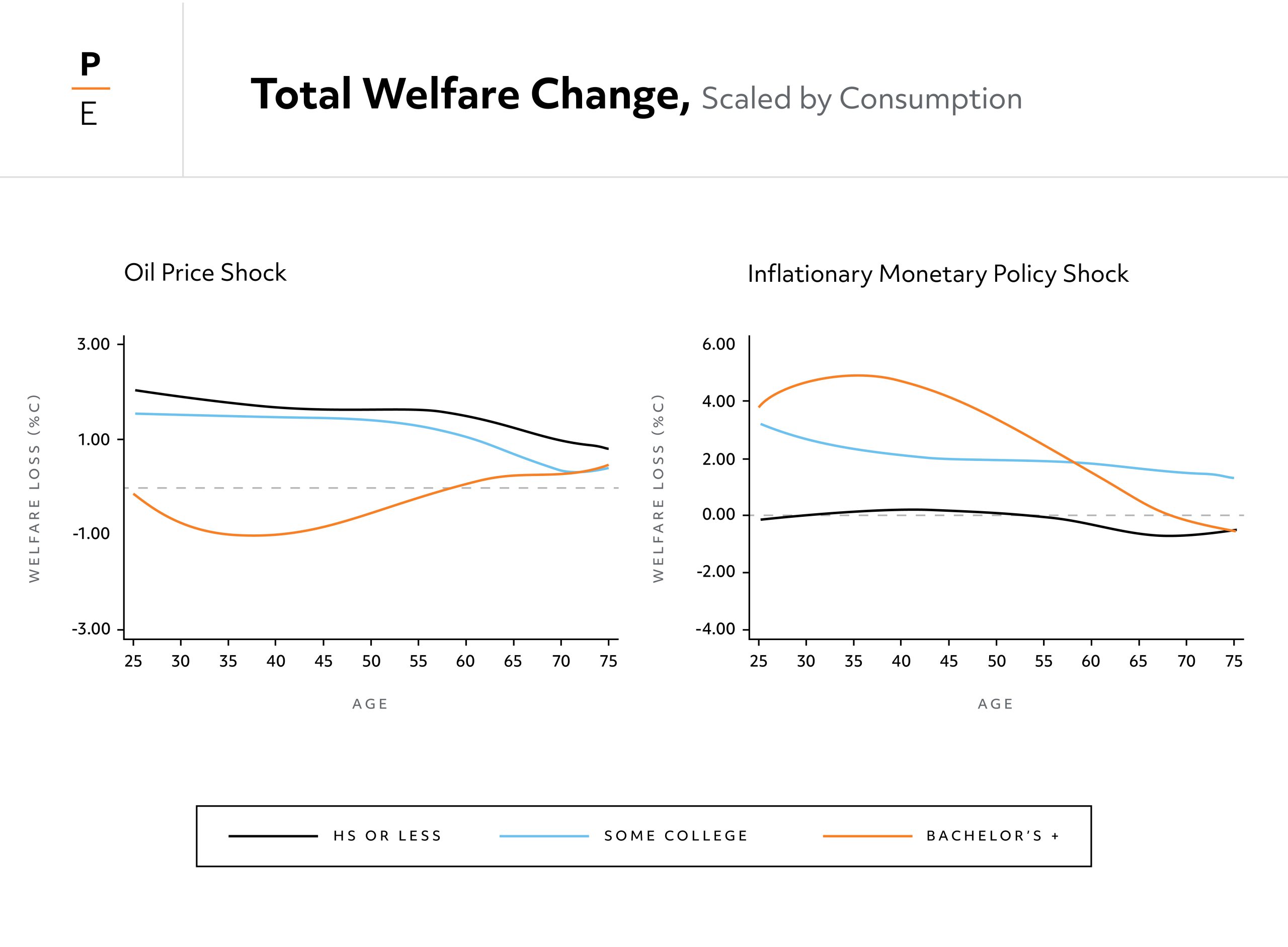

The authors find that these different sources of inflation carry radically different distributional consequences. Inflation that results from an oil shock is generally regressive, hitting middle-aged households with lower levels of education the hardest. In contrast, inflation that results from expansionary monetary policy shock is generally progressive.

After a one standard deviation oil price increase, those with less than a high school education must be paid around $800 (around 2% of annual consumption) in 2019 to be able to afford their pre-shock level of utility. Meanwhile, middle-aged, college-educated households gain the equivalent of $833 (1.1% of annual consumption) from the oil price increase.

In a monetary policy shock, a quarter-point rate cut has little effect on low-education households, while middle-aged, high-education households lose around $4,000 dollars (5.5% of annual consumption).

To understand these overall distributional consequences, the authors study a range of effects on households, including whether inflation pushes up the prices of products a household consumes more than it pushes up their income. The new model takes into account the price of the goods the household purchases, the wage income the household earns, the dividend stream on the assets owned by the household, the prices of assets that the household trades, and transfer income from the government.

Ultimately, the authors find that the effects of a shock on asset prices are the major reason oil shocks are regressive and expansionary monetary shocks are progressive. Oil supply contractions lead to big declines in equity prices (and minimally affect the price of bonds or housing), making it easier for middle-aged households with a college education to buy equities at a low price. Monetary expansions do the opposite, raising the prices of equities and housing, ultimately hurting middle-aged households who would be buying those assets, especially those with a college education.

Other effects impact winners and losers, but by a much smaller margin. Both shocks raise the price of oil, which hurts low-education houses most. This nudges both shocks toward regressivity before factoring in the effects on asset prices.

In terms of effects on jobs and wages, oil shocks increase unemployment and reduce the weekly earnings of those who are employed. These effects are most notable among low-education households, but relatively small overall. Expansionary monetary policy shocks have the opposite effect, decreasing unemployment and increasing weekly earnings, especially for the lowest-education households. But overall, these effects on jobs and earnings hurt households throughout the distribution (with the exception of older households who rely less on labor income to begin with) and do little to make the shock overwhelming progressive or regressive.

A major contribution of the research is that it provides a new way for researchers to model how a particular inflationary shock in the real world may affect different groups of people based on a wide range of inputs.

The authors’ framework combines cross-sectional data on household consumption (the BLS’ Consumer Expenditure Survey), labor income (CPS panel data), transfer income (for example payments from TANF, Social Security, veterans pensions, and more), household balance sheets and estimated asset holdings (SCF survey data) with impulse response functions estimated using standard time series techniques.

The authors then aggregate the impulse response functions to determine the welfare effects of inflationary oil price and monetary shocks. In doing so, they produce new empirical findings on these shocks.

Ultimately, the analysis demonstrates that, in terms of distributional consequences, all inflationary periods are not created equal. To understand the true effects of inflation on welfare across the distribution, researchers must take into account the source of inflation and measure how changes in the cost of living for a given household compare to changes in household income.